U.S. Bancorp and BNY Mellon

Brighter Days Ahead?

Although they’re very different banks, I’ve lumped together U.S. Bancorp and BNY Mellon for this write-up. By my estimates, both investments have performed pretty poorly for Berkshire to date. We’re not talking about a super immaterial figure either - entering 2022, Berkshire’s aggregate investment in these two (at cost) was over $8 billion. Both positions have been trimmed at times, so overall Berkshire has invested a bit more between the two.

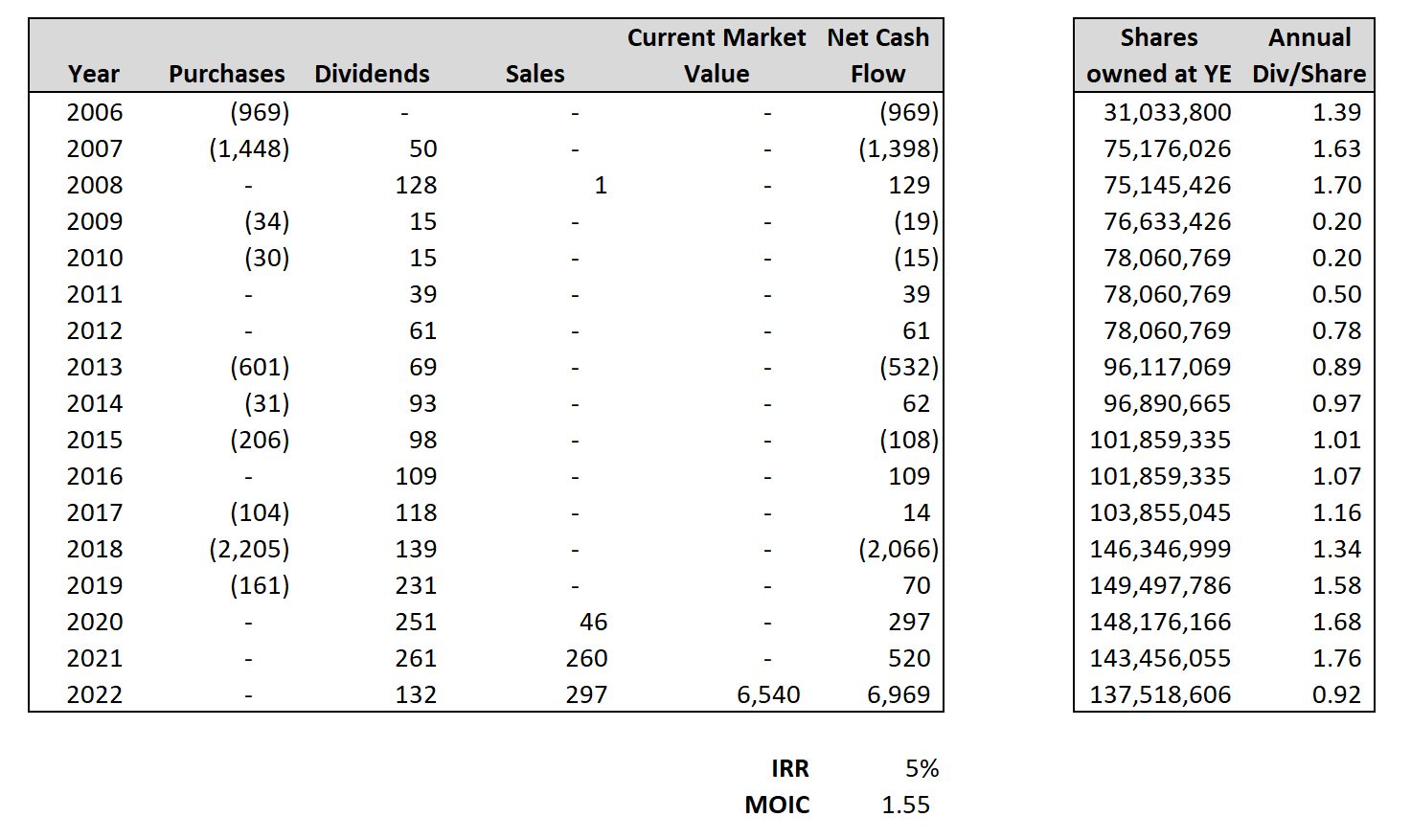

Let’s start with U.S. Bancorp, whose primary business is to accept deposits and make loans, for both individuals and small and large businesses. It is comparable to Wells Fargo in that it is primarily a commercial bank, although a lot smaller. Berkshire built up its sizable position between 2006 and 2019, at the end of which they owned 149.5 million shares at a cost of $5.7 billion (~$38 per share). They’ve trimmed shares during 2020-2022, but still own 137.5 million shares as of Q2 2022. At the time of writing, U.S. Bancorp was trading around $48 per share. I’ve estimated the IRR to date to be around 5%, with the MOIC around 1.55. Had I run this analysis in January, the IRR would be closer to 7% and the MOIC closer to 2.

Bank of New York Mellon is a much more complex bank. It was actually founded in 1784 by Alexander Hamilton and was the first company listed on the New York Stock Exchange. Today, is it primarily a custodian bank, generating most of its revenue from various management and investment fees (rather than from net interest income like US Bank). At the end of 2021 they had $46.7 trillion in assets under custody (not a typo).

Berkshire bought some shares of BNY Mellon in 2010 and 2012-2013, trimmed some for a nice gain in 2014-2015, and then really enlarged the position during 2016-2018. By the end of 2018, Berkshire owned 84.5 million shares at a cost of $3.9 billion (~$46 per share). During 2019-2020, they trimmed the position down to 66.8 million shares. The stock currently trades around $44 per share. By my estimates, the IRR to date is just 2% and the MOIC is 1.10. However, if I had run my analysis in January 2022, when the stock was $63, the IRR would be 8% and the MOIC 1.43.

For each bank, I’ve compiled some metrics below, including return on tangible equity (the average of 2019-2021), price-to-tangible book value, price to earnings (using average earnings from 2019-2021), dividend yield, and annualized change in share count over the ten-year period ending 12/31/2021. Both appear to be high-quality (given their high-teens ROEs) banks trading at reasonable prices, with a history of returning meaningful amounts of cash to shareholders via dividends and buybacks. To date, Berkshire’s investments in these two have done poorly. However, given today’s valuations, I struggle to see how these two deliver anything worse than a high-single-digits return to Berkshire going forward.