American Express

A 70-year on-and-off relationship

According to his 1994 letter to Berkshire Hathaway shareholders, Warren Buffett’s association with American Express dates back to 1953. At 23 years old, he began buying shares of Investors Diversified Services (IDS), a financial planning company that was rapidly growing and trading at just 3x earnings (as Buffett writes, “[t]here was a lot of low-hanging fruit in those days”). He wrote a long report about the stock and sold it for $1 as a Wall Street Journal ad. In 1979, IDS was bought by Alleghany Corporation (which ironically was just acquired by Berkshire in 2022), and then in 1984 it was sold by Alleghany to Amex. In the early 1990s, when Berkshire built its position in Amex, IDS was responsible for about a third of Amex’s earnings.

Buffett’s history with Amex continued in the mid-1960s, when Buffett was running Buffett Partnership. He put about 40% (!) of the fund’s capital into Amex following the salad oil scandal. To briefly summarize, an Amex subsidiary had attested to the legitimacy of the salad oil inventories of its client Allied Crude Vegetable Oil. When it was discovered that Allied Crude’s inventories were fraudulently overstated, Amex’s stock fell 50% due to uncertainty about its future legal liabilities. Once the legal liabilities were settled, the stock rallied, scoring Buffett a multi-bagger over a 3-year period for his partners.1

Berkshire Hathaway’s association with Amex began in 1991, when they invested $300 million into American Express preferred shares that paid an 8.85% dividend ($26.55M). In 1994, Berkshire converted the preferreds into common shares and purchased additional common shares for $424 million. They kept buying in 1995 ($669 million) and topped off the position in 1997 ($77 million). The total cost basis was $1.47 billion, or $9.70 per split-adjusted share.

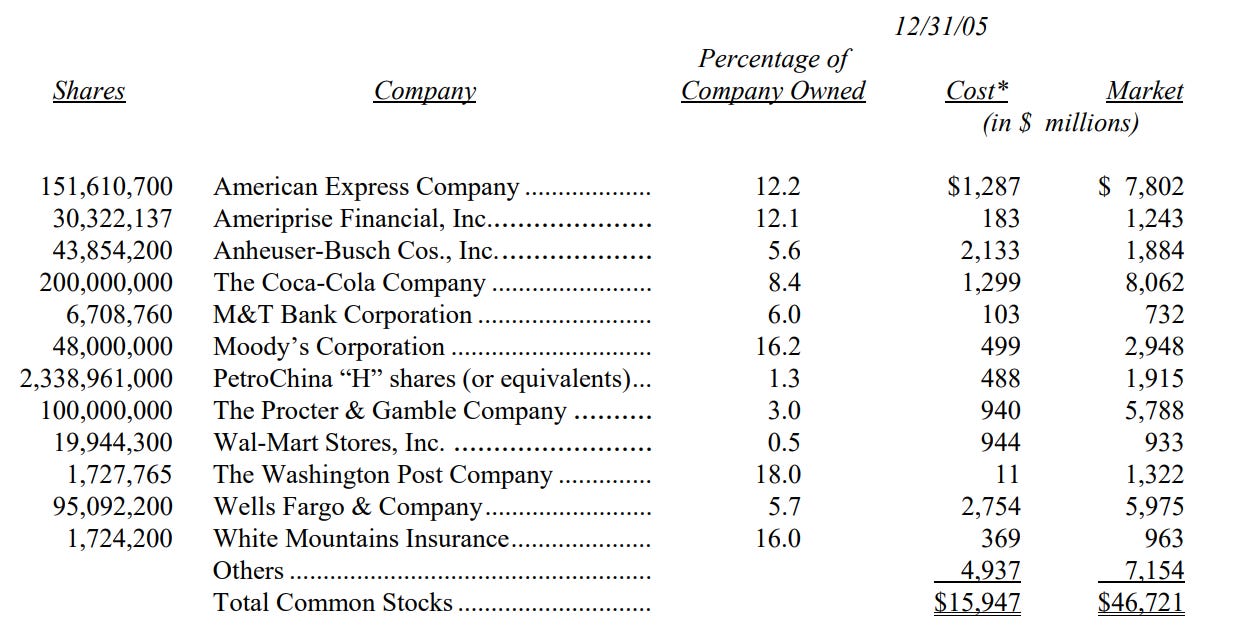

Buffett’s recent shareholder letters show a different cost basis ($1.29 billion), but the same amount of split-adjusted shares owned as 1997 - why? In 2005, Amex spun off IDS, which was renamed “Ameriprise Financial”. Below is an excerpt from the 2005 letter showing how the original $1.47 billion cost basis was broken out Amex and Ameriprise. Berkshire sold all of its Ameriprise shares during 2006-2008, and I estimate that they pocketed around $1.5 billion.

Below is a breakdown of the entire investment to date. Berkshire invested $1.47 billion between 1991 and 1997. To date they’ve collected ~$3.2 billion in dividends, pocketed ~$1.5 billion from the Ameriprise spin-off & subsequent sales, and the current position is worth ~$23 billion. I’ve estimated the IRR to be about 14% and the MOIC to be 19.

If anybody knows where I can find exact numbers behind this trade, please let me know